The month you claim Social Security decides what every month pays.

Whenwise shows your estimated check at every claiming age from 62 to 70, computed with the Social Security Administration’s published 2026 formula, on your iPhone, in under a minute. No account. No email. No SSN.

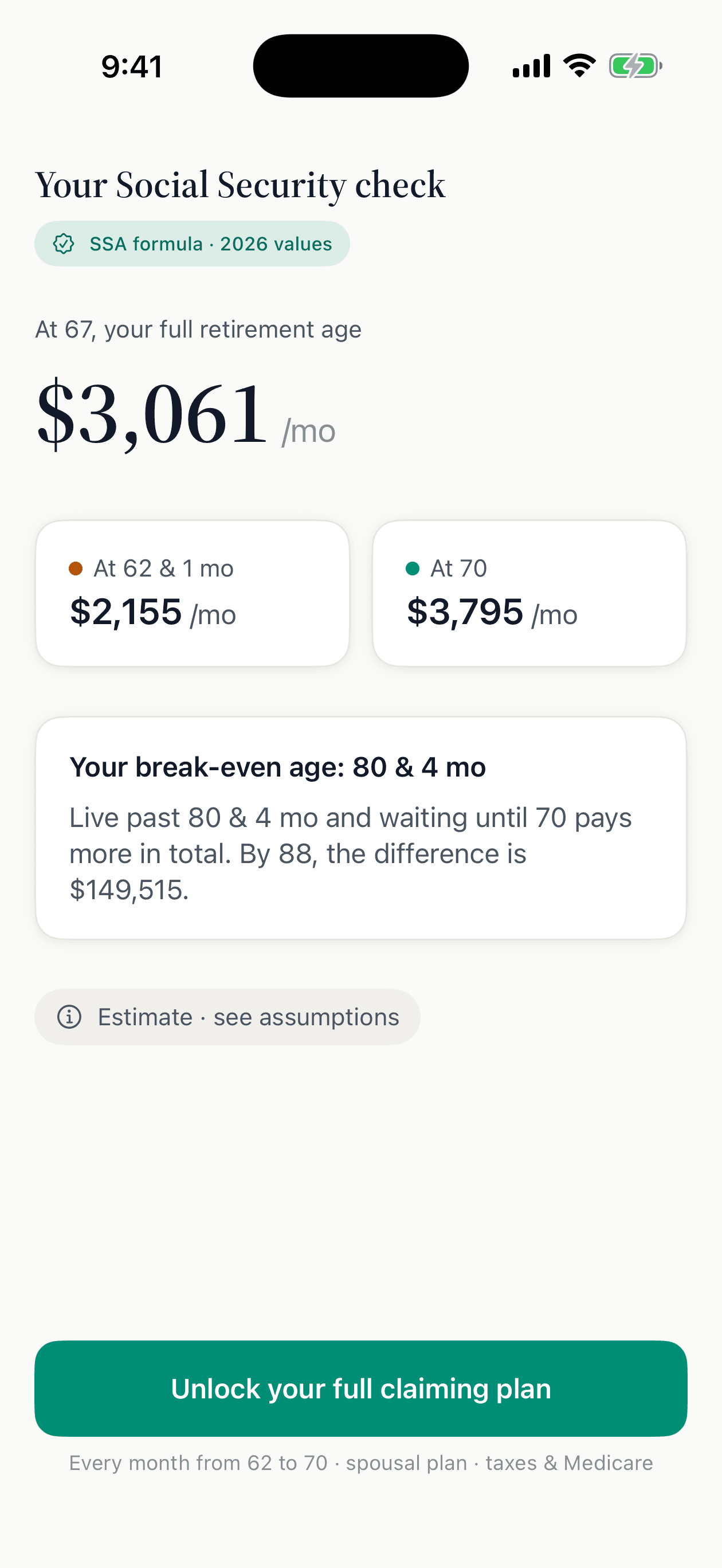

SSA formula · 2026 values · every number traces to a public source

Slide the age. Watch the check.

Every month from 62 to 70 pays a different amount: $2,155 becomes $3,795 for the example worker below, and waiting is worth $188,875 through age 90. The app does this with your numbers.

Claiming at 67

$3,061a month

+$906 vs claiming at 62 + 1 mo

Example: born June 1962, earned $90,000 last year, works until 67. Estimates in today’s dollars, computed with SSA’s published 2026 formula by the same engine that powers the app. Your numbers come from your own earnings record.

A plan, not a one-time answer.

1

Start with two facts

Your birth date and last year’s earnings. That’s enough for your first estimate. Or import your SSA statement file and Whenwise uses your actual earnings record, read entirely on your iPhone.

2

See every month, 62 to 70

Your check at every claiming age, your break-even age, spousal benefits for both of you, and what you keep after taxes and Medicare, each number labeled with its assumptions and sources.

3

Stay current until you file

Claiming is a years-long decision with dated deadlines: your Medicare window, your full-retirement-age month, the age-70 cap. Whenwise keeps your plan current with fresh SSA numbers every October, until the day you file.

Private: nothing leaves your iPhone.

No account. No email. No Social Security number. Whenwise has no server: your birth date, earnings, and imported statement stay on your device. The App Store privacy label reads “Data Not Collected.”

Whenwise is independent and is not affiliated with, endorsed by, or connected to the Social Security Administration.

Built for the decision, not just the number.

Every claiming month

Slide from 62 to 70 and compare all 96 months, with your break-even age and what waiting is worth over your lifetime.

Spousal benefits, finally clear

Both checks, every combination of claiming ages, and exactly how the spousal top-up works for your household.

What you actually keep

Federal benefit taxation and Medicare IRMAA awareness, so the number you plan on is the number that arrives.

Your real earnings record

Import the statement file from your my Social Security account. It's read on your iPhone and never leaves it.

Advisor-ready PDF report

A clean, sourced report of your claiming picture you can print, share, or bring to a professional.

Fresh numbers every October

When SSA announces the new year's values, your plan updates, current until the day you file.

Fair questions, straight answers.

When should I take Social Security?

There's no single right age, and anyone who says otherwise is selling something. Claiming at 62 means a smaller check for more years; waiting toward 70 means a larger check for fewer years. If you expect a long retirement, waiting usually pays more in total. If you need the income sooner, or your health says don't bet on the late years, claiming earlier can be the sound choice. Whenwise shows your numbers both ways. The choice stays yours.

How much bigger is my check if I wait?

Claiming before your full retirement age reduces your check by five-ninths of one percent per month for the first 36 months and five-twelfths of one percent for each month beyond that: about a 30% cut at 62 for anyone born in 1960 or later. Waiting past full retirement age adds 8% per year in delayed retirement credits until 70. For a worker born in June 1962 who earned $90,000 last year, that's an estimated $2,155 a month at 62 versus $3,795 at 70, computed with SSA's published 2026 formula.

Is Social Security running out? Should I claim early before it's cut?

Social Security isn't going away. Its trustees project the retirement fund can pay full benefits until about 2033; after that, payroll taxes still cover roughly three quarters of benefits unless Congress acts, and Congress has acted before every past deadline. Claiming early to get ahead of a shortfall locks in a smaller check for life, and any future fix would likely apply to early and late claimers alike. (Source: the Trustees Report at ssa.gov.)

What does my spouse get?

A husband or wife can receive up to half of the higher earner's full-retirement-age amount, if that's more than their own benefit. Social Security pays their own benefit first and tops it up to the spousal ceiling. Whenwise's Couple tab shows both checks side by side, for every combination of claiming ages.

Is Whenwise part of Social Security?

No. Whenwise is independent: not affiliated with, endorsed by, or connected to the Social Security Administration. We compute with SSA's published formulas and values, and every number traces to a public source. For official decisions, confirm with SSA.

Where does my information go?

Nowhere. Your answers and your imported statement stay on your iPhone. There's no account, no email sign-up, and Whenwise never asks for your Social Security number. The App Store privacy label reads “Data Not Collected.” Delete the app and your information goes with it.

More depth: when to take Social Security, the free break-even calculator, and how every number is computed.

Six figures ride on one date. See yours.

Your check at 62, 67, and 70, in under a minute, private by design.